Navigating Impact and Return

Everyone knows clean tech investment has been on a tear. What fewer people know is - when it comes to specific environmental impact and financial returns, various segments of the clean tech sector have proven far from equal.

According to the Clean Investment Monitor, which tracks global flows, global clean tech capital commitments tripled over the past seven years, reaching a total of nearly $2 trillion by end-2025. Societal priorities as well as the confidence investors have placed in the sector have driven rapid growth.

As capital commitments to a wide range of climate tech solutions have increased, however, their tangible environmental impacts and return spectrums have broadened. In particular, there has been a wide financial return divergence between technologies which promote operational efficiency and cost savings, on the one hand, versus those in direct power generation, on the other. Understanding the dynamics driving this range of outcomes and, in particular, the dispersion of returns across various technology segments, could help inform successful, future allocations.

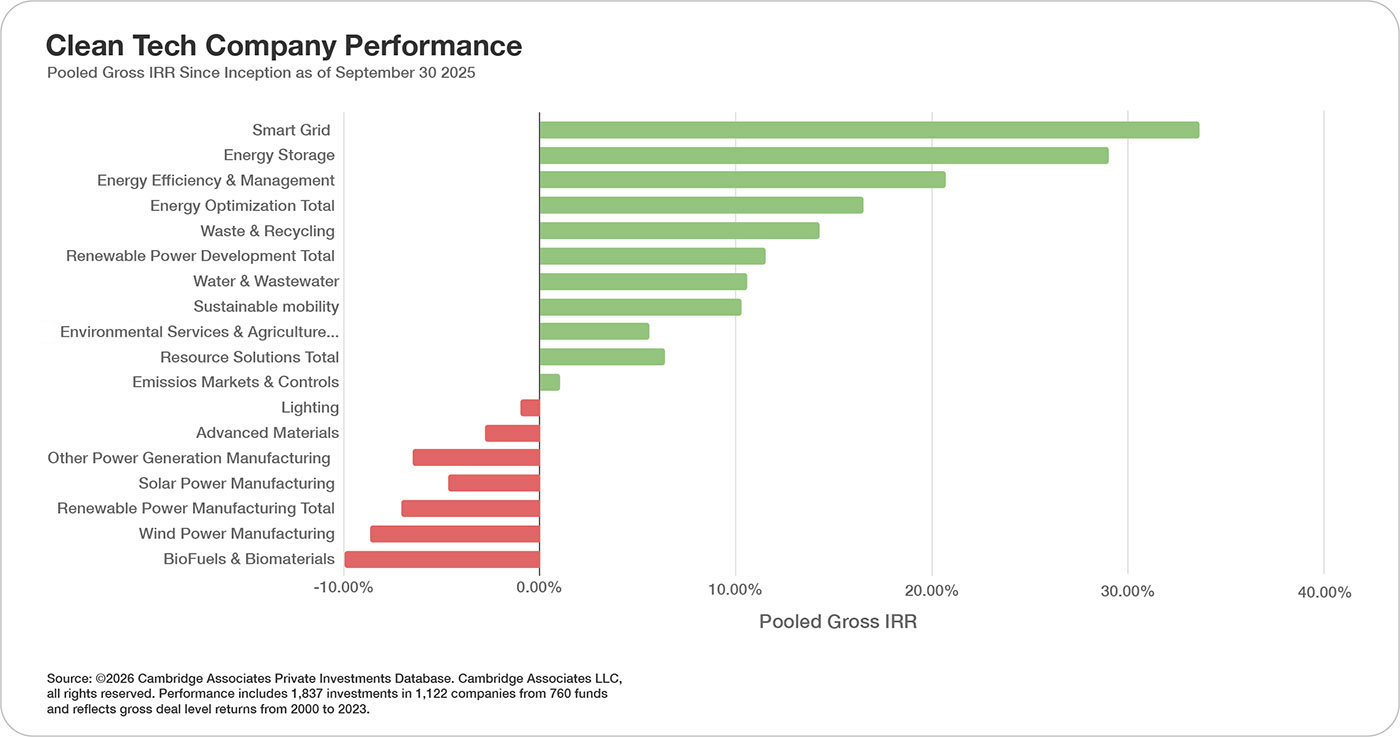

Boston based investment consultant Cambridge Associates tracks private market investment returns for private deals across 18 sectors of clean tech. Their data base covers 1,837 private investments in 1,122 companies and over 760 funds from 2000-2023. Private market valuations are subject to greater variability than public markets as they are often based on unrealized measurements.

Their reported results will surprise many, beginning with the most well-known sectors. Cambridge data shows that most deals involving renewable infrastructure manufacturing, the highest profile segment, have on average generated negative returns. Specifically, Cambridge reports that from 2020-2023 Solar Power Manufacturing and Wind Power Manufacturing generated single-digit losses (-4.7%, -8.7%) while Bio-Fuels, another popular sector, have also generated negative -10.0%.

In contrast to these losses in renewables, most other climate strategies have had positive returns. According to Cambridge, Smart Grid, Energy Storage and Energy Efficiency and Management have generated sizable returns, with an IRR of 33.7%, 29.1%, 20.7% respectively. Renewable Power Development - distinct from renewable infrastructure manufacturing - has had similarly respectable returns of 11.5%. Waste and Recycling, and Energy Optimization also scored positive double-digit IRRs since inception through their reporting period: 14.3% and 16.3% respectively. These returns are well in excess of broad stock market indices over the same period.

As with all impact investments, financial returns are only part of the clean tech investment story. To be properly evaluated, all impact investment strategies should be weighed across three dimensions: risk, return and impact. We do not believe there are any axiomatic tradeoffs between return impact, something the Cambridge data also demonstrates.

This said, we recognize that many investors - particularly those with allocations to early stage, catalytic capital - are more than willing to accept lower returns in exchange for specific social and environmental improvements. Those tradeoffs should be clearly understood and – ideally – quantified and agreed to in advance, wherever possible. For example, some financially underperforming clean tech sectors - such as Environmental Services and Agriculture Solutions, which delivered 5.6% on average for the period - may be adequate for some capital owners given their specific non-financial goals for land reclamation and/or species preservation.

"Many lessons have been learned during that journey. Perhaps the most important are that sub-sector returns beneath the broad category of “climate investing” are widely divergent"

For double bottom line impact investors who prioritize returns pari passu with positive climate outcomes, or for those who do not want to make any financial concessions, picking the right business in the right sector has never been more crucial for success.

Climate tech has come a long way since the early 2000s. Many lessons have been learned during that journey. Perhaps the most important are that sub-sector returns beneath the broad category of “climate investing” are widely divergent, and a monolithic allocation to the theme could produce sub-optimal results. As we enter a new energy cycle with oil prices spiking and military uncertainty around the Strait of Hormuz, we are reminded both how dependent the global economy remains upon the fossil fuel economy, and how vulnerable that industry is to geopolitical ruptures. Given energy independence at the national level is becoming more urgent, many home-grown clean tech investments will get a second look.

Investors in clean tech must discern what their goals are and how the strategies they are considering are likely to deliver on those specific objectives. In this transformative and still evolving field, sector specification, manager selection, and long-term value creation matter now more than ever.